Code

import pandas as pd

df_train = pd.read_csv("datasets/AMZN_train.csv")The task is to predict the day price direction of Amazon.com, Inc. (AMZN).

The stock market is very complex and highly volatile. In order to be profitable, we do not need to predict the correct price, but rather, the price direction: whether it will be higher or lower than the price that is today. If we predict it to be higher, we might as well buy some stocks, else, we should probably sell. Therefore, the target would be a binary classification whether the next day closing price will be higher than the opening price.

We have data for the period from 1997 up to the year 2020 that we have split into training (1997-2016), validation (2016-2018) and testing (2018-2020) periods. The data is available in the AMZN_train.csv, AMZN_val.csv and AMZN_test.csv files, respectively.

import pandas as pd

df_train = pd.read_csv("datasets/AMZN_train.csv")df_train| Date | Open | High | Low | Close | Adj Close | Volume | |

|---|---|---|---|---|---|---|---|

| 0 | 1997-05-15 | 2.437500 | 2.500000 | 1.927083 | 1.958333 | 1.958333 | 72156000 |

| 1 | 1997-05-16 | 1.968750 | 1.979167 | 1.708333 | 1.729167 | 1.729167 | 14700000 |

| 2 | 1997-05-19 | 1.760417 | 1.770833 | 1.625000 | 1.708333 | 1.708333 | 6106800 |

| 3 | 1997-05-20 | 1.729167 | 1.750000 | 1.635417 | 1.635417 | 1.635417 | 5467200 |

| 4 | 1997-05-21 | 1.635417 | 1.645833 | 1.375000 | 1.427083 | 1.427083 | 18853200 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 4776 | 2016-05-09 | 673.950012 | 686.979980 | 671.409973 | 679.750000 | 679.750000 | 3982200 |

| 4777 | 2016-05-10 | 694.000000 | 704.549988 | 693.500000 | 703.070007 | 703.070007 | 6105600 |

| 4778 | 2016-05-11 | 705.789978 | 719.000000 | 701.650024 | 713.229980 | 713.229980 | 7338200 |

| 4779 | 2016-05-12 | 717.380005 | 722.450012 | 711.510010 | 717.929993 | 717.929993 | 5048200 |

| 4780 | 2016-05-13 | 714.640015 | 719.250000 | 706.510010 | 709.919983 | 709.919983 | 4763400 |

4781 rows × 7 columns

df_train.shape(4781, 7)df_train.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 4781 entries, 0 to 4780

Data columns (total 7 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Date 4781 non-null object

1 Open 4781 non-null float64

2 High 4781 non-null float64

3 Low 4781 non-null float64

4 Close 4781 non-null float64

5 Adj Close 4781 non-null float64

6 Volume 4781 non-null int64

dtypes: float64(5), int64(1), object(1)

memory usage: 261.6+ KBdf_train.describe()| Open | High | Low | Close | Adj Close | Volume | |

|---|---|---|---|---|---|---|

| count | 4781.000000 | 4781.000000 | 4781.000000 | 4781.000000 | 4781.000000 | 4.781000e+03 |

| mean | 127.619845 | 129.480122 | 125.697925 | 127.662449 | 127.662449 | 8.225935e+06 |

| std | 145.693083 | 147.132537 | 144.053633 | 145.677581 | 145.677581 | 7.810188e+06 |

| min | 1.406250 | 1.447917 | 1.312500 | 1.395833 | 1.395833 | 4.872000e+05 |

| 25% | 34.299999 | 34.849998 | 33.660000 | 34.310001 | 34.310001 | 4.200900e+06 |

| 50% | 62.880001 | 64.750000 | 60.937500 | 62.750000 | 62.750000 | 6.200100e+06 |

| 75% | 189.009995 | 191.600006 | 186.210007 | 189.029999 | 189.029999 | 9.239900e+06 |

| max | 717.380005 | 722.450012 | 711.510010 | 717.929993 | 717.929993 | 1.043292e+08 |

df_train["Date"].describe()count 4781

unique 4781

top 1997-05-15

freq 1

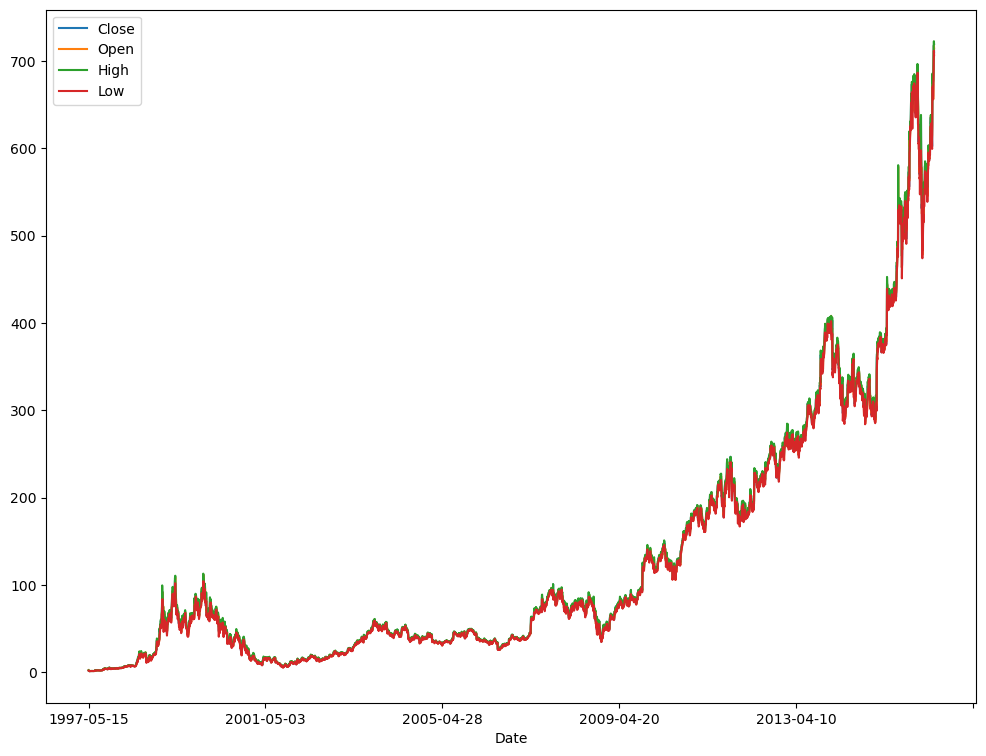

Name: Date, dtype: objectdf_train["Date"].min(), df_train["Date"].max()('1997-05-15', '2016-05-13')from matplotlib import pyplot as plt

plt.rcParams["figure.figsize"] = (12, 9)_ = df_train.plot(x="Date", y=["Close", "Open", "High", "Low"])

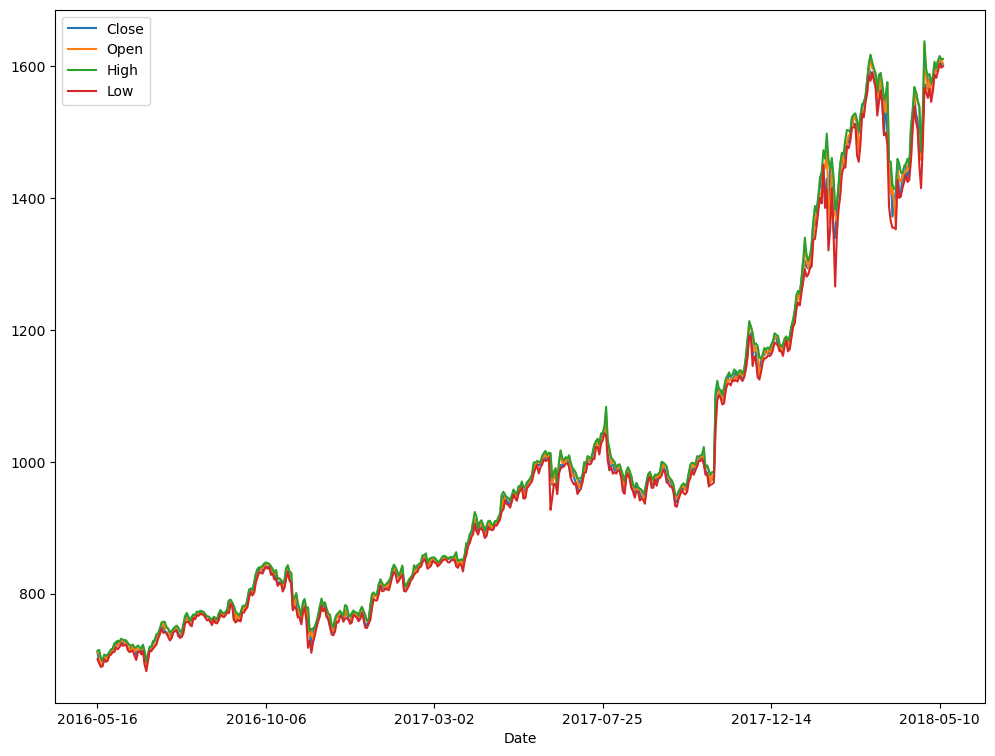

We would like to repeat the same analysis for the validation and testing set, to make sure that they follow a similar distribution and that there are no surprising errors there. We create a function to do that.

def analyse(dataframe):

"""Runs an exploration analysis of the dataframe."""

print("Shape", dataframe.shape, "\n")

print("Columns", dataframe.columns, "\n")

dataframe.info()

print("\n", dataframe.describe(), "\n")

print("The data ranges from", dataframe["Date"].min(), "to", dataframe["Date"].max())

dataframe.plot(x="Date", y=["Close", "Open", "High", "Low"])# read validation and test sets and then analyse them

df_val = pd.read_csv("datasets/AMZN_val.csv")

analyse(df_val)Shape (503, 7)

Columns Index(['Date', 'Open', 'High', 'Low', 'Close', 'Adj Close', 'Volume'], dtype='object')

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 503 entries, 0 to 502

Data columns (total 7 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Date 503 non-null object

1 Open 503 non-null float64

2 High 503 non-null float64

3 Low 503 non-null float64

4 Close 503 non-null float64

5 Adj Close 503 non-null float64

6 Volume 503 non-null int64

dtypes: float64(5), int64(1), object(1)

memory usage: 27.6+ KB

Open High Low Close Adj Close \

count 503.000000 503.000000 503.000000 503.000000 503.000000

mean 992.201292 999.898131 982.574513 991.828966 991.828966

std 255.496588 259.220381 250.100614 254.885469 254.885469

min 689.559998 696.820007 682.119995 691.359985 691.359985

25% 780.500000 785.625000 772.410004 780.294983 780.294983

50% 948.000000 954.400024 941.140015 948.229980 948.229980

75% 1125.349976 1131.750000 1120.369995 1126.500000 1126.500000

max 1634.010010 1638.099976 1603.439941 1609.079956 1609.079956

Volume

count 5.030000e+02

mean 3.918924e+06

std 2.069197e+06

min 1.458800e+06

25% 2.655050e+06

50% 3.324800e+06

75% 4.469000e+06

max 1.656500e+07

The data ranges from 2016-05-16 to 2018-05-14

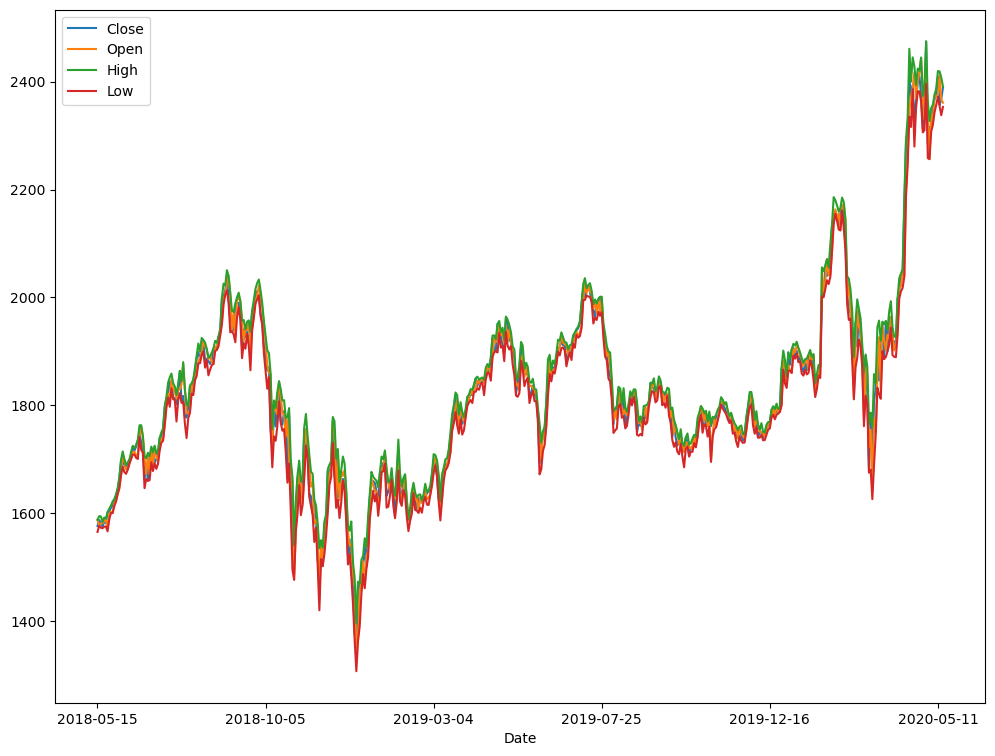

df_test = pd.read_csv("datasets/AMZN_test.csv")

analyse(df_test)Shape (504, 7)

Columns Index(['Date', 'Open', 'High', 'Low', 'Close', 'Adj Close', 'Volume'], dtype='object')

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 504 entries, 0 to 503

Data columns (total 7 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Date 504 non-null object

1 Open 504 non-null float64

2 High 504 non-null float64

3 Low 504 non-null float64

4 Close 504 non-null float64

5 Adj Close 504 non-null float64

6 Volume 504 non-null int64

dtypes: float64(5), int64(1), object(1)

memory usage: 27.7+ KB

Open High Low Close Adj Close \

count 504.000000 504.000000 504.000000 504.000000 504.000000

mean 1823.927758 1843.069246 1803.067065 1824.040536 1824.040536

std 178.129809 179.294163 177.457741 178.470078 178.470078

min 1346.000000 1396.030029 1307.000000 1343.959961 1343.959961

25% 1712.924988 1730.602447 1691.637543 1713.642517 1713.642517

50% 1806.539978 1824.244995 1791.289978 1806.119995 1806.119995

75% 1908.154968 1921.580048 1887.580017 1902.842468 1902.842468

max 2443.199951 2475.000000 2396.010010 2474.000000 2474.000000

Volume

count 5.040000e+02

mean 4.705042e+06

std 2.288185e+06

min 8.813000e+05

25% 3.078725e+06

50% 4.068450e+06

75% 5.763300e+06

max 1.556730e+07

The data ranges from 2018-05-15 to 2020-05-14

Once we have done our exploration of the data, we can move on to the predictive modeling part of the task. The task was to predict if the next day’s closing price will be higher than the opening price. We do not have that information explicitly in our data, so we have to infer it.

This is relatively simple, we just need to compare the closing and opening prices one day in advance.

To achieve that, first, we will make sure that the data is sorted by the date. We can use the sort_values method and pass in the Date column as a parameter, sorting it in ascending order.

Next, we need to shift the DataFrame by one row / one day and compare the prices. Pandas has a method for doing exactly that, the shift method. We specify a period of minus one (so that we shift the data from the next day back). Because it is a logical operation, Pandas would return a True / False result for each comparison. We want this to be presented as 1 / 0 for the machine learning models, so we will map it to type int. To store all of this information, we will create a new column, called Target.

df_train.sort_values(by="Date", inplace=True)

df_val.sort_values(by="Date", inplace=True)

df_test.sort_values(by="Date", inplace=True)# notice that we shift by a period of '-1', this takes the next day's price direction for the current day

# a positive period will take the days from the past

df_train["Target"] = (df_train["Close"] > df_train["Open"]).shift(periods=-1, fill_value=0).astype(int)df_train| Date | Open | High | Low | Close | Adj Close | Volume | Target | |

|---|---|---|---|---|---|---|---|---|

| 0 | 1997-05-15 | 2.437500 | 2.500000 | 1.927083 | 1.958333 | 1.958333 | 72156000 | 0 |

| 1 | 1997-05-16 | 1.968750 | 1.979167 | 1.708333 | 1.729167 | 1.729167 | 14700000 | 0 |

| 2 | 1997-05-19 | 1.760417 | 1.770833 | 1.625000 | 1.708333 | 1.708333 | 6106800 | 0 |

| 3 | 1997-05-20 | 1.729167 | 1.750000 | 1.635417 | 1.635417 | 1.635417 | 5467200 | 0 |

| 4 | 1997-05-21 | 1.635417 | 1.645833 | 1.375000 | 1.427083 | 1.427083 | 18853200 | 0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 4776 | 2016-05-09 | 673.950012 | 686.979980 | 671.409973 | 679.750000 | 679.750000 | 3982200 | 1 |

| 4777 | 2016-05-10 | 694.000000 | 704.549988 | 693.500000 | 703.070007 | 703.070007 | 6105600 | 1 |

| 4778 | 2016-05-11 | 705.789978 | 719.000000 | 701.650024 | 713.229980 | 713.229980 | 7338200 | 1 |

| 4779 | 2016-05-12 | 717.380005 | 722.450012 | 711.510010 | 717.929993 | 717.929993 | 5048200 | 0 |

| 4780 | 2016-05-13 | 714.640015 | 719.250000 | 706.510010 | 709.919983 | 709.919983 | 4763400 | 0 |

4781 rows × 8 columns

df_train["Target"].value_counts()Target

1 2392

0 2389

Name: count, dtype: int64df_val["Target"] = (df_val["Close"] > df_val["Open"]).shift(periods=-1, fill_value=0).astype(int)

df_val["Target"].value_counts()Target

0 255

1 248

Name: count, dtype: int64df_test["Target"] = (df_test["Close"] > df_test["Open"]).shift(periods=-1, fill_value=0).astype(int)

df_test["Target"].value_counts()Target

1 255

0 249

Name: count, dtype: int64df_train["Moving_Average_3"] = (df_train["Close"] - df_train["Open"]).rolling(window=3, min_periods=1).mean()

df_val["Moving_Average_3"] = (df_val["Close"] - df_val["Open"]).rolling(window=3, min_periods=1).mean()

df_test["Moving_Average_3"] = (df_test["Close"] - df_test["Open"]).rolling(window=3, min_periods=1).mean()df_train["Moving_Average_7"] = (df_train["Close"] - df_train["Open"]).rolling(window=7, min_periods=1).mean()

df_val["Moving_Average_7"] = (df_val["Close"] - df_val["Open"]).rolling(window=7, min_periods=1).mean()

df_test["Moving_Average_7"] = (df_test["Close"] - df_test["Open"]).rolling(window=7, min_periods=1).mean()# current price direction

df_train["Today_Direction"] = df_train["Close"] - df_train["Open"]

df_val["Today_Direction"] = df_val["Close"] - df_val["Open"]

df_test["Today_Direction"] = df_test["Close"] - df_test["Open"]# price range

df_train["Price_Range"] = df_train["High"] - df_train["Low"]

df_val["Price_Range"] = df_val["High"] - df_val["Low"]

df_test["Price_Range"] = df_test["High"] - df_test["Low"]df_train.sample(10, random_state=42)| Date | Open | High | Low | Close | Adj Close | Volume | Target | Moving_Average_3 | Moving_Average_7 | Today_Direction | Price_Range | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2895 | 2008-11-14 | 43.610001 | 44.500000 | 41.500000 | 41.750000 | 41.750000 | 11949700 | 0 | -0.253335 | -0.601429 | -1.860001 | 3.000000 |

| 4430 | 2014-12-22 | 301.940002 | 307.359985 | 301.940002 | 306.540009 | 306.540009 | 4003800 | 0 | 0.436666 | -0.705710 | 4.600007 | 5.419983 |

| 3618 | 2011-09-29 | 234.169998 | 234.300003 | 216.289993 | 222.440002 | 222.440002 | 9378500 | 0 | -6.126663 | -2.434283 | -11.729996 | 18.010010 |

| 763 | 2000-05-24 | 46.437500 | 49.750000 | 40.437500 | 48.562500 | 48.562500 | 11666600 | 0 | -0.937500 | -0.580357 | 2.125000 | 9.312500 |

| 4392 | 2014-10-28 | 289.760010 | 298.000000 | 289.760010 | 295.589996 | 295.589996 | 5572600 | 0 | 4.253326 | 2.681423 | 5.829986 | 8.239990 |

| 4657 | 2015-11-16 | 640.919983 | 649.989990 | 622.289978 | 647.809998 | 647.809998 | 7435900 | 0 | -7.243347 | -0.264299 | 6.890015 | 27.700012 |

| 4008 | 2013-04-22 | 259.350006 | 264.600006 | 258.029999 | 263.549988 | 263.549988 | 2119100 | 1 | -0.343333 | -0.287140 | 4.199982 | 6.570007 |

| 555 | 1999-07-29 | 51.187500 | 52.187500 | 50.000000 | 50.781250 | 50.781250 | 18748000 | 0 | -0.841146 | -0.713170 | -0.406250 | 2.187500 |

| 2754 | 2008-04-28 | 80.639999 | 82.500000 | 80.120003 | 81.970001 | 81.970001 | 10991900 | 0 | 1.453336 | 1.212857 | 1.330002 | 2.379997 |

| 33 | 1997-07-02 | 1.515625 | 1.593750 | 1.510417 | 1.588542 | 1.588542 | 3882000 | 1 | 0.026042 | 0.004464 | 0.072917 | 0.083333 |

# this is the target column that we aim to predict

y_col = "Target"

# these are the input features for the models

X_cols = [

"Open",

"Close",

"High",

"Low",

"Volume",

"Adj Close",

"Today_Direction",

"Price_Range",

"Moving_Average_3",

"Moving_Average_7"

]X_train = df_train[X_cols]

y_train = df_train[y_col]

X_val = df_val[X_cols]

y_val = df_val[y_col]

X_test = df_val[X_cols]

y_test = df_val[y_col]# for reproducibility

RANDOM_SEED = 42from sklearn.linear_model import LogisticRegression

from sklearn.preprocessing import StandardScaler

from sklearn.metrics import RocCurveDisplay

# use default parameters

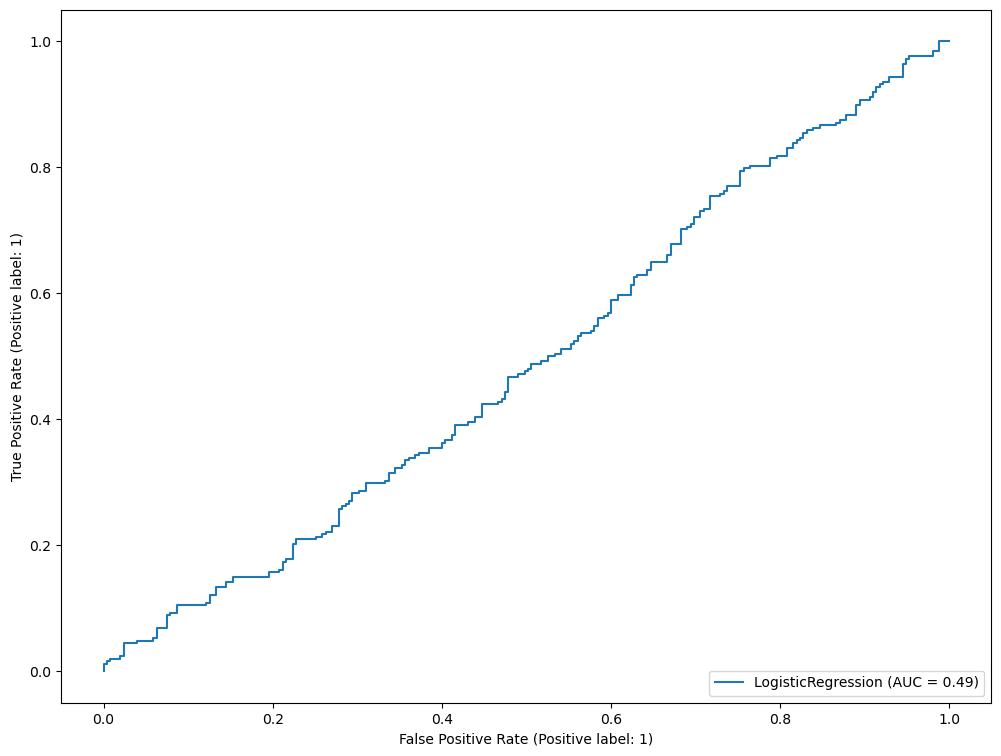

lr = LogisticRegression()

# fit to train set

lr.fit(X_train, y_train)

# plot ROC curve, and show AUC for the validation set

RocCurveDisplay.from_estimator(lr, X_val, y_val)

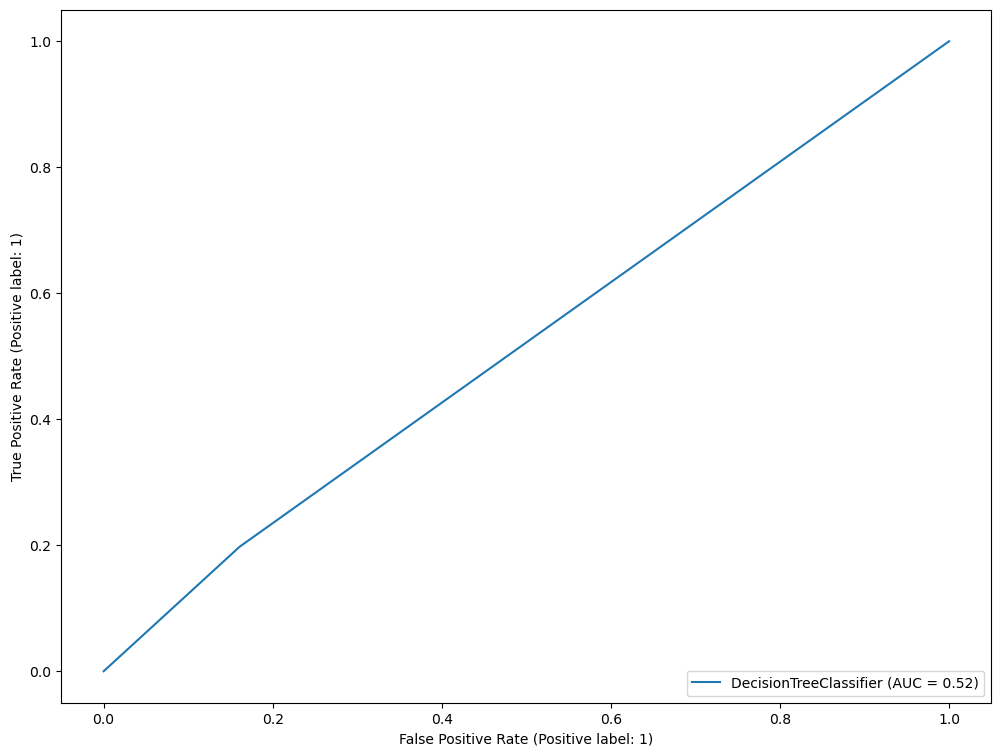

from sklearn.tree import DecisionTreeClassifier

# remember to use the random seed to be able to reproduce the same results

dt = DecisionTreeClassifier(random_state=RANDOM_SEED)

dt.fit(X_train, y_train)

RocCurveDisplay.from_estimator(dt, X_val, y_val)

#RocCurveDisplay.from_estimator

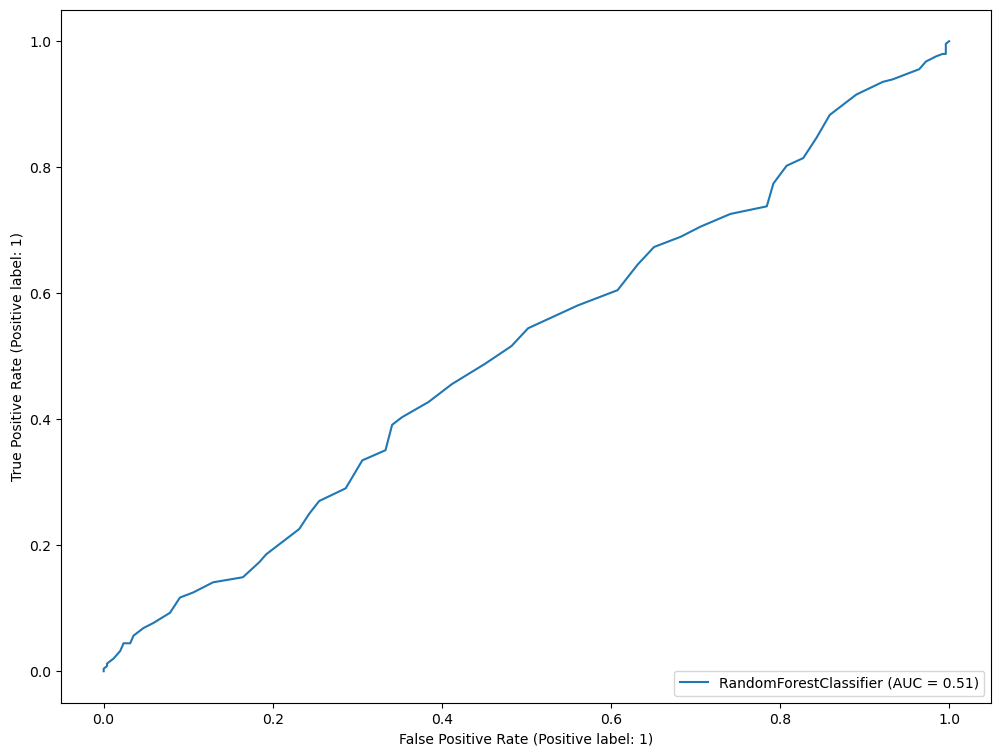

from sklearn.ensemble import RandomForestClassifier

rf = RandomForestClassifier(random_state=RANDOM_SEED)

rf.fit(X_train, y_train)

RocCurveDisplay.from_estimator(rf, X_val, y_val)

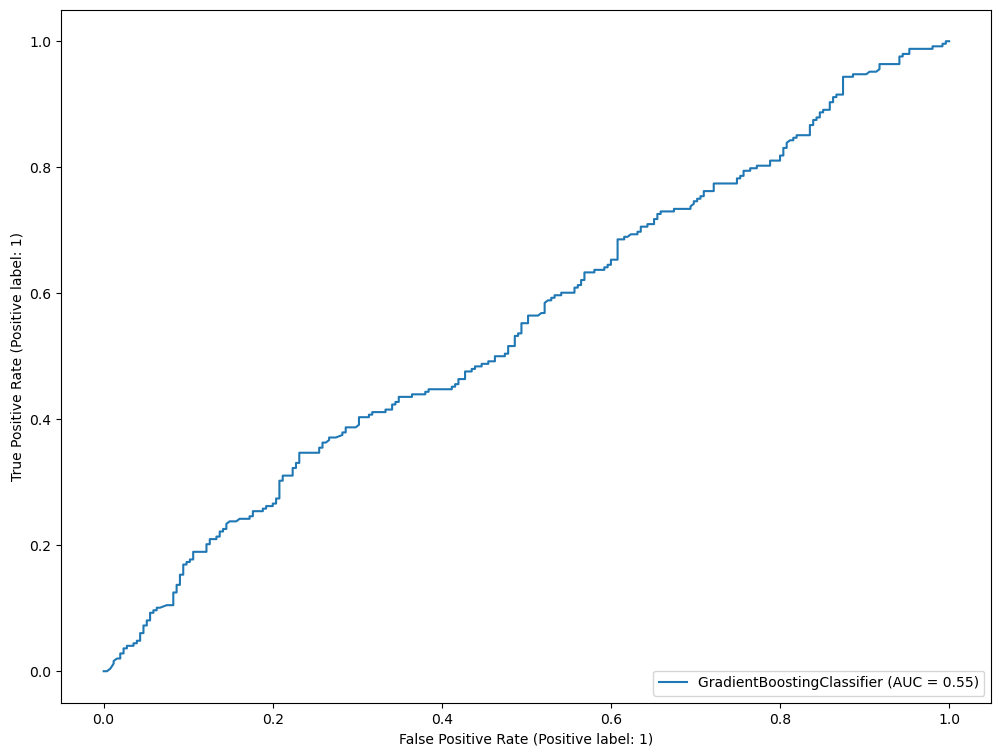

from sklearn.ensemble import GradientBoostingClassifier

gb = GradientBoostingClassifier(random_state=RANDOM_SEED)

gb.fit(X_train, y_train)

RocCurveDisplay.from_estimator(gb, X_val, y_val)

import tensorflow as tf

# set seed for reproducibility of results

tf.random.set_seed(RANDOM_SEED)

print("Tensorflow version", tf.__version__)Tensorflow version 2.11.0model = tf.keras.models.Sequential([

tf.keras.layers.Normalization(axis=-1),

tf.keras.layers.Dense(10, input_shape=[X_train.shape[1],], activation="relu", kernel_initializer='random_normal', bias_initializer='zeros'),

tf.keras.layers.Dropout(0.2, seed=RANDOM_SEED),

tf.keras.layers.Dense(5, activation="relu", kernel_initializer='random_normal', bias_initializer='zeros'),

tf.keras.layers.Dense(1, activation="sigmoid", kernel_initializer='random_normal', bias_initializer='zeros')

])# this configures the model's loss function, weight optimizer, and metrics to keep track of

model.compile(

loss="binary_crossentropy",

optimizer=tf.keras.optimizers.Adam(),

metrics=['AUC']

)def learning_rate_scheduler(epoch, learning_rate):

"""Learning rate decay callback."""

if epoch < 5:

return learning_rate

else:

return learning_rate * tf.math.exp(-0.01)

early_stopping_callback = tf.keras.callbacks.EarlyStopping(patience=10, verbose=1, restore_best_weights=True)

learning_rate_callback = tf.keras.callbacks.LearningRateScheduler(learning_rate_scheduler)# the model.fit(...) method returns a 'history' object with stats about the training

history = model.fit(

x=X_train,

y=y_train,

validation_data=(X_val, y_val),

epochs=50,

verbose=1,

callbacks=[early_stopping_callback, learning_rate_callback])Epoch 1/50

150/150 [==============================] - 1s 1ms/step - loss: 54.1560 - auc: 0.4979 - val_loss: 0.7589 - val_auc: 0.4888 - lr: 0.0010

Epoch 2/50

150/150 [==============================] - 0s 603us/step - loss: 1.9100 - auc: 0.5104 - val_loss: 0.6956 - val_auc: 0.4786 - lr: 0.0010

Epoch 3/50

150/150 [==============================] - 0s 589us/step - loss: 0.9015 - auc: 0.4972 - val_loss: 0.7808 - val_auc: 0.5095 - lr: 0.0010

Epoch 4/50

150/150 [==============================] - 0s 585us/step - loss: 0.7510 - auc: 0.5277 - val_loss: 0.6962 - val_auc: 0.4864 - lr: 0.0010

Epoch 5/50

150/150 [==============================] - 0s 592us/step - loss: 0.7006 - auc: 0.5049 - val_loss: 0.6948 - val_auc: 0.4911 - lr: 0.0010

Epoch 6/50

150/150 [==============================] - 0s 584us/step - loss: 0.7013 - auc: 0.5044 - val_loss: 0.6931 - val_auc: 0.5058 - lr: 9.9005e-04

Epoch 7/50

150/150 [==============================] - 0s 571us/step - loss: 0.6936 - auc: 0.5015 - val_loss: 0.6931 - val_auc: 0.5022 - lr: 9.8020e-04

Epoch 8/50

150/150 [==============================] - 0s 572us/step - loss: 0.6936 - auc: 0.4869 - val_loss: 0.6932 - val_auc: 0.4944 - lr: 9.7045e-04

Epoch 9/50

150/150 [==============================] - 0s 562us/step - loss: 0.6934 - auc: 0.4909 - val_loss: 0.6931 - val_auc: 0.5000 - lr: 9.6079e-04

Epoch 10/50

150/150 [==============================] - 0s 553us/step - loss: 0.6932 - auc: 0.4993 - val_loss: 0.6931 - val_auc: 0.5000 - lr: 9.5123e-04

Epoch 11/50

150/150 [==============================] - 0s 556us/step - loss: 0.6932 - auc: 0.4916 - val_loss: 0.6931 - val_auc: 0.5000 - lr: 9.4176e-04

Epoch 12/50

150/150 [==============================] - 0s 552us/step - loss: 0.6932 - auc: 0.5020 - val_loss: 0.6931 - val_auc: 0.5000 - lr: 9.3239e-04

Epoch 13/50

150/150 [==============================] - 0s 558us/step - loss: 0.6932 - auc: 0.4954 - val_loss: 0.6931 - val_auc: 0.5000 - lr: 9.2312e-04

Epoch 14/50

150/150 [==============================] - 0s 539us/step - loss: 0.6932 - auc: 0.5000 - val_loss: 0.6931 - val_auc: 0.5000 - lr: 9.1393e-04

Epoch 15/50

150/150 [==============================] - 0s 547us/step - loss: 0.6932 - auc: 0.5000 - val_loss: 0.6932 - val_auc: 0.5000 - lr: 9.0484e-04

Epoch 16/50

118/150 [======================>.......] - ETA: 0s - loss: 0.6932 - auc: 0.5000Restoring model weights from the end of the best epoch: 6.

150/150 [==============================] - 0s 575us/step - loss: 0.6932 - auc: 0.5000 - val_loss: 0.6932 - val_auc: 0.5000 - lr: 8.9583e-04

Epoch 16: early stoppingmodel.summary()Model: "sequential"

_________________________________________________________________

Layer (type) Output Shape Param #

=================================================================

normalization (Normalizatio (None, 10) 21

n)

dense (Dense) (None, 10) 110

dropout (Dropout) (None, 10) 0

dense_1 (Dense) (None, 5) 55

dense_2 (Dense) (None, 1) 6

=================================================================

Total params: 192

Trainable params: 171

Non-trainable params: 21

_________________________________________________________________from matplotlib import pyplot as plt

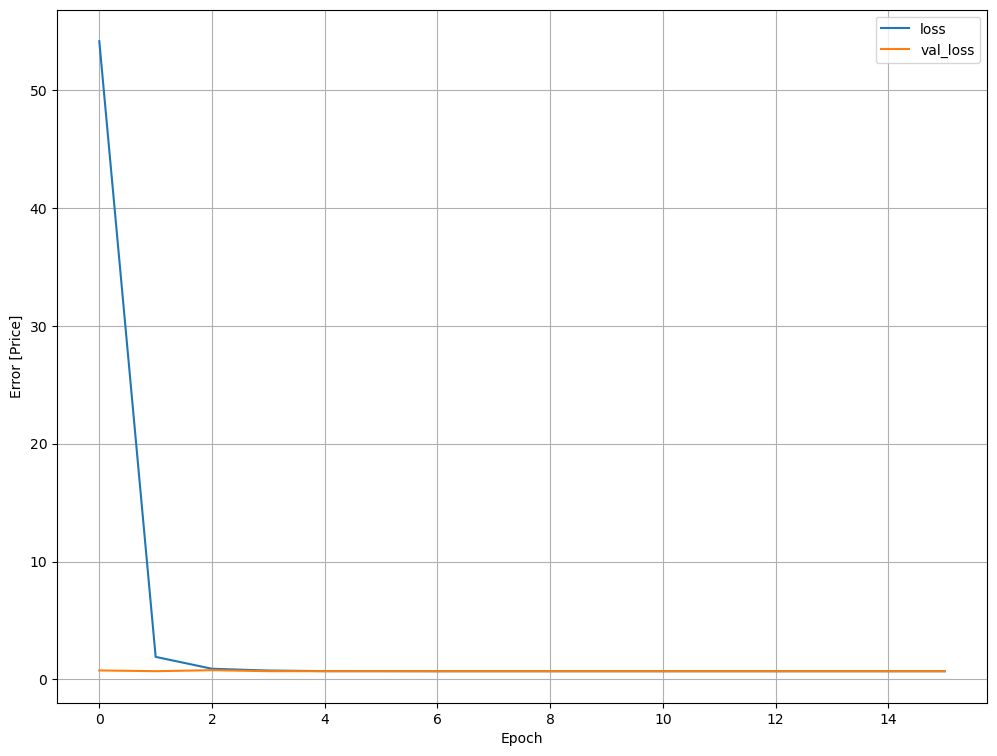

plt.plot(history.history['loss'], label='loss')

plt.plot(history.history['val_loss'], label='val_loss')

plt.xlabel('Epoch')

plt.ylabel('Error [Price]')

plt.legend()

plt.grid(True)

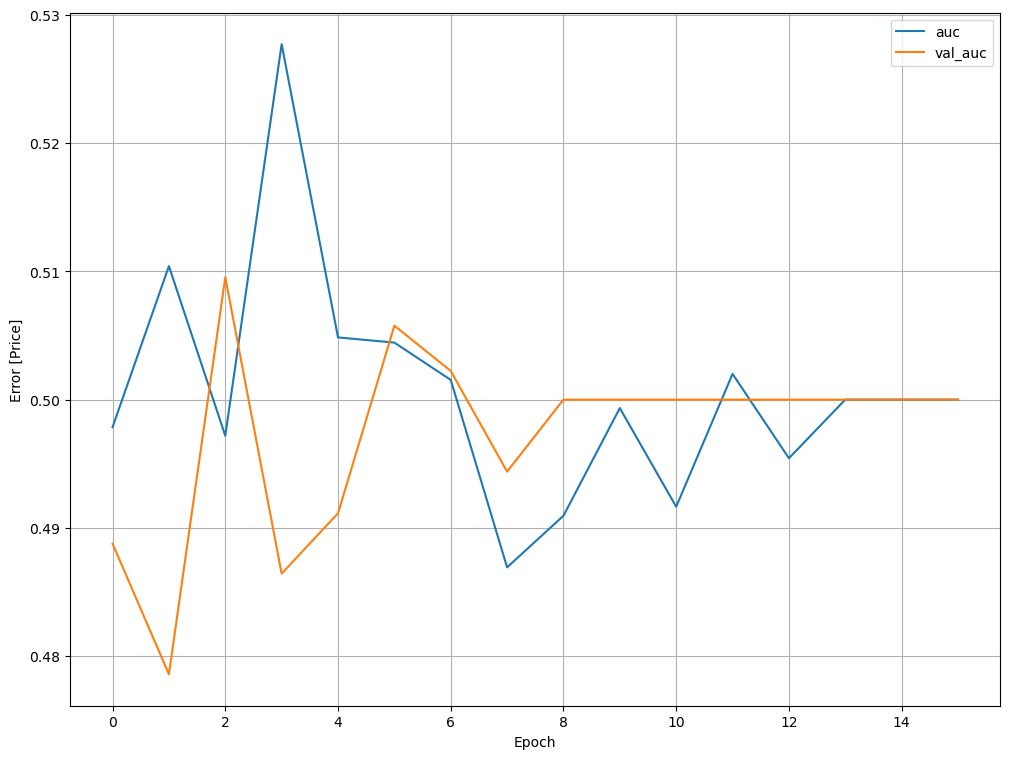

plt.plot(history.history['auc'], label='auc')

plt.plot(history.history['val_auc'], label='val_auc')

plt.xlabel('Epoch')

plt.ylabel('Error [Price]')

plt.legend()

plt.grid(True)

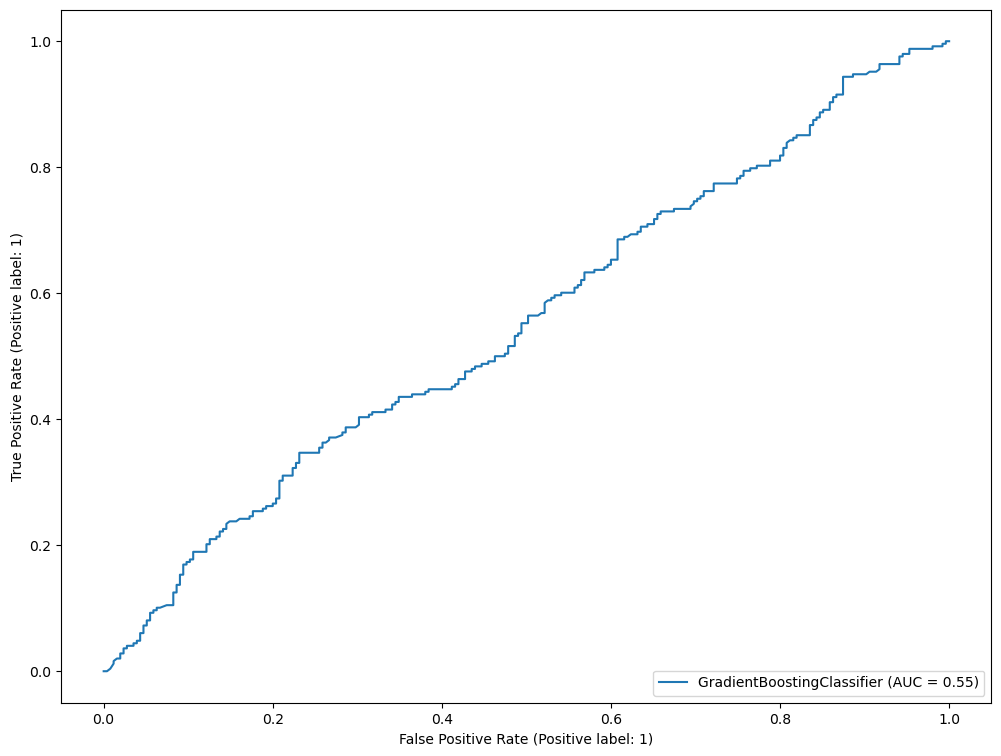

The gradient boosting classifier provided the best AUC score on the validation set. It is a common machine learning practice to train multiple models on the same train/validation data set and provide a model that works best. To simulate a production environment, we have held the test set aside until now.

RocCurveDisplay.from_estimator(gb, X_test, y_test)

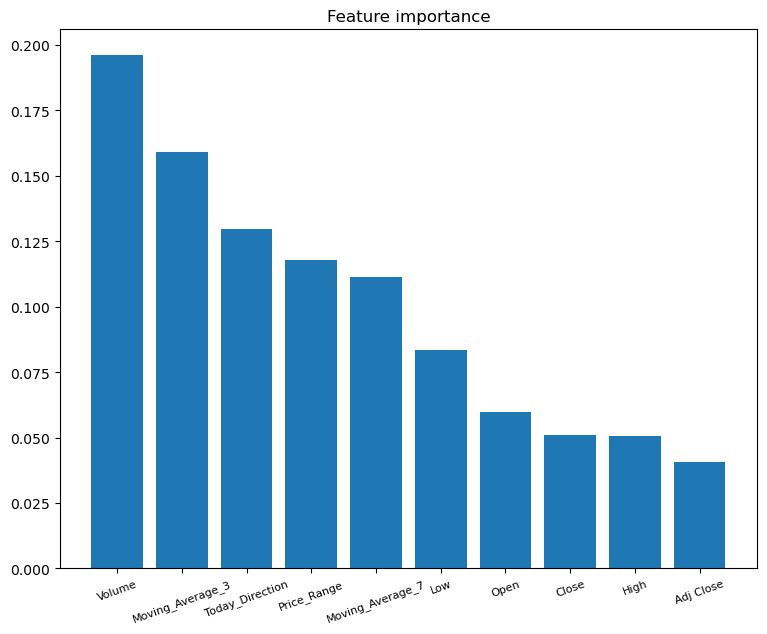

import numpy as np

# Calculate feature importances

importances = gb.feature_importances_

# Sort feature importances in descending order

indices = np.argsort(importances)[::-1]

# Rearrange feature names so they match the sorted feature importances

names = [df_train[X_cols].columns[i] for i in indices]

_ = plt.figure(figsize=(9, 7))

plt.bar(names, importances[indices])

_ = plt.title("Feature importance")

_ = plt.xticks(rotation=20, fontsize = 8)